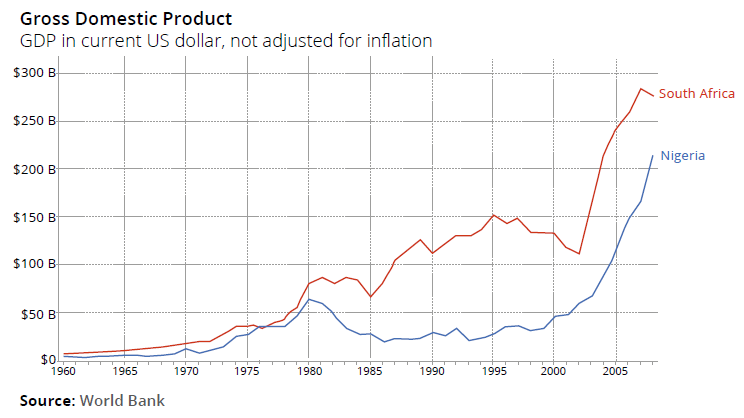

Once the continent’s strongest economy, Nigeria continues to experience one of the worst recessions it has encountered in over 20 years. With growth still subdued, largely the result of long-depressed oil prices, the country remains in a fairly precarious position – one exacerbated by a chronic shortage of hard currencies, which has forced many of the country’s largest companies in a broad range of sectors to scale back on new investment. Against that backdrop, the country’s capital markets have been relatively anaemic, with the local currency bond market largely remaining the reprieve of the nation’s banks, blue-chip corporates, and states.

With fresh reforms and a broad increase in the price of oil on the horizon, the government will need to keep economic diversification, new investment into infrastructure, and prudent monetary and fiscal policy at the top of its priority list if it is to help Nigeria return to a position of strength.

To Be Frank: 2016 Was Rough

In marked contrast to part performance, the Nigerian economy spent much of 2016 in the doldrums, hampered by inflation, a lack of FX reserves, and the low price of oil – the country’s main export. Analysts suspect the country’s economy shrank between about 1.6% and 1.7% year on year in 2016, driven largely by losses from oil and the oil related sectors, agriculture and manufacturing – which account for roughly 19%, 18% and 9% of total economic output, respectively, according to the National Bureau of Statistics. The declines differ sharply with nearly 3% growth recorded in 2015.

The oil sector reflected the bulk of the deceleration. Oil and oil-related services were down 22.1% year on year during the third quarter of 2016, up slightly from 17.1% declines seen during the second quarter, according to figures from OPEC, the Nigerian National Petroleum Corporation, and Standard Bank. This contrasts with the scale of the declines seen in non-oil areas of the economy; non-oil sectors contracted by just 0.03% during the third quarter of 2016, a slight improvement from the 0.36% contraction seen in the previous quarter.

The oil sector reflected the bulk of the deceleration. Oil and oil-related services were down 22.1% year on year during the third quarter of 2016, up slightly from 17.1% declines seen during the second quarter, according to figures from OPEC, the Nigerian National Petroleum Corporation, and Standard Bank. This contrasts with the scale of the declines seen in non-oil areas of the economy; non-oil sectors contracted by just 0.03% during the third quarter of 2016, a slight improvement from the 0.36% contraction seen in the previous quarter.

Nigeria’s manufacturing sector has also been vulnerable to some of the country’s economic challenges, with supply chains severely affected by a chronic shortage of hard currencies needed to import raw materials and intermediate goods, as well as infrastructure bottlenecks including power supply deficits. The manufacturing sector contracted by 4.38% in the third quarter of 2016, according to government figures.

The agricultural sectors have continued to contribute positive GDP growth, despite a slowdown to more moderate levels over the past year. The sector grew by 4.88% in the third quarter of 2016 according to government figures, but that sharply down from quarterly growth levels of over 13% seen during the same period in 2014.

The service sectors, which account for about 53% of the Nigeria’s GPD, saw a wide range of variance driven by a multitude of factors. For instance, the information and telecommunications (ICT) sector put in upwards of 9.6% growth in the third quarter of 2016, driven in part by increased demand from growing numbers of small and medium-sized enterprises. The leisure and tourism sectors, on the other hand reported steep drop-offs, contracting 4.6% in the second half of last year – driven by concerns around security, particularly in the northern part of the country, and due to stagnant real incomes, which also drove declines in construction and the residential real estate sectors.

Against that backdrop, the current account balance moved from a deficit of roughly US$15.4bn at the end of 2015 to a surplus of just over US$1bn through the first half of 2016, according to Standard Bank research, driven in part by a contraction in services and income – and despite a massive drop in the price of oil during that 18-month period.

Against that backdrop, the current account balance moved from a deficit of roughly US$15.4bn at the end of 2015 to a surplus of just over US$1bn through the first half of 2016, according to Standard Bank research, driven in part by a contraction in services and income – and despite a massive drop in the price of oil during that 18-month period.

FDI inflows halved over the past year, falling from US$4.5bn in 2015 to just US$1.8bn in 2016. Analysts at FBN Quest believe that if the Central Bank of Nigeria is unable to stabilise the naira – which it has struggled to do since it partially floated the currency in June 2016 – and if oil prices continue to remain weak the current account deficit could rise as high as US$14.6bn, or 3.1% of GDP, in 2017.

Credit markets have felt the pain. Bond yields have reflected mounting risk, as have trading volumes. Average yields on Nigeria’s local-currency 10-year government bonds climbed from just over 11% in January 2016 to touch 16.4% in March 2017, while the sovereign’s Eurobonds continue to trade between the 6.75% and 8.2% range depending on tenor. Turnover in local fixed income market trading, meanwhile, has steadily improved since its December 2015 lows. Monthly trading volume shifted abruptly from its 18-month peak of NGN7.95tn in October 2015 to NGN2.61tn in December 2015, but climbed back to as high as NGN6.85tn in December 2016 before settling at NGN6.34tn in January 2017, according to data from FMDQ, an OTC securities exchange. Bank credit has become more expensive, particularly hard-currency credit, while non-performing loans in the banking system have pushed past 5% of all outstanding loan books.

While 2016 was a difficult year to say the least, we also maintain that 2017 is likely to see a broad uplift in the country’s fortunes. Nigeria’s oversubscribed US$1bn Eurobond has helped extend import coverage to nearly 5-months, giving the country some much needed breathing room to reassess how it addresses its FX challenges and builds up further reserves without weighing on inflation; demand for the bond has also confirmed the sovereign is unlikely to struggle sourcing external financing in the near term, easing concerns that it could double up on the local market and put pressure on liquidity and rates. With security being restored in many parts of the north east of the country over the past year, analysts expect broad improvements in productivity in the region. Improving oil prices – coupled with more ambitious average daily production targets planned for the following two years – will be broadly supportive of the economy, not just the oil and oil-related sectors. The government’s medium-term reform plan, meanwhile, is likely to give the economy a much-needed boost.

While 2016 was a difficult year to say the least, we also maintain that 2017 is likely to see a broad uplift in the country’s fortunes. Nigeria’s oversubscribed US$1bn Eurobond has helped extend import coverage to nearly 5-months, giving the country some much needed breathing room to reassess how it addresses its FX challenges and builds up further reserves without weighing on inflation; demand for the bond has also confirmed the sovereign is unlikely to struggle sourcing external financing in the near term, easing concerns that it could double up on the local market and put pressure on liquidity and rates. With security being restored in many parts of the north east of the country over the past year, analysts expect broad improvements in productivity in the region. Improving oil prices – coupled with more ambitious average daily production targets planned for the following two years – will be broadly supportive of the economy, not just the oil and oil-related sectors. The government’s medium-term reform plan, meanwhile, is likely to give the economy a much-needed boost.