Investors often mistake the asset class as having the same risk-premium as to the United States (US) or European (EU) high yield (HY) corporate bonds, but the risks are fundamentally different. EM sovereign debt offers geographical and macro-economic diversification. Furthermore, sovereign debt investors are backed by a more robust legal framework that minimises loss given default in unfortunate incidents.

The persistent mispricing of EM sovereign debt is partially due to broad ownership from ‘tourist investors’. In our opinion their biases, prejudices and limited ability to analyse the credits can lead to an excessive risk premium. Lastly, supply and demand dynamics favour EM sovereign debt over the long term. Most large long-term investors remain structurally underweight in an asset class where they should be structurally invested and using sell-off as opportunities to go overweight.

Asset Allocators are Long-Distance Runners

Last year, for the first time in history, an athlete managed to run a marathon in under two hours. The historical mark was achieved by Eliud Kipchoge, a Kenyan marathoner, in a performance marking the culmination of years of training, personal sacrifice and teamwork. Bankers and asset managers are often keen long-distance runners. After all, like investing, distance running demands planning, disciplined training and precise execution while dealing with exogenous (weather) and endogenous (injuries) adversities. The ‘Holy Grail’ of long-term investing is identifying assets that perform like Mr Kipchoge: Not quite as explosive as Usain Bolt in the 100 and 200 metre-sprint, but still quite fast and steady over the long run.

EM Sovereign Debt: A Long-Term Champion

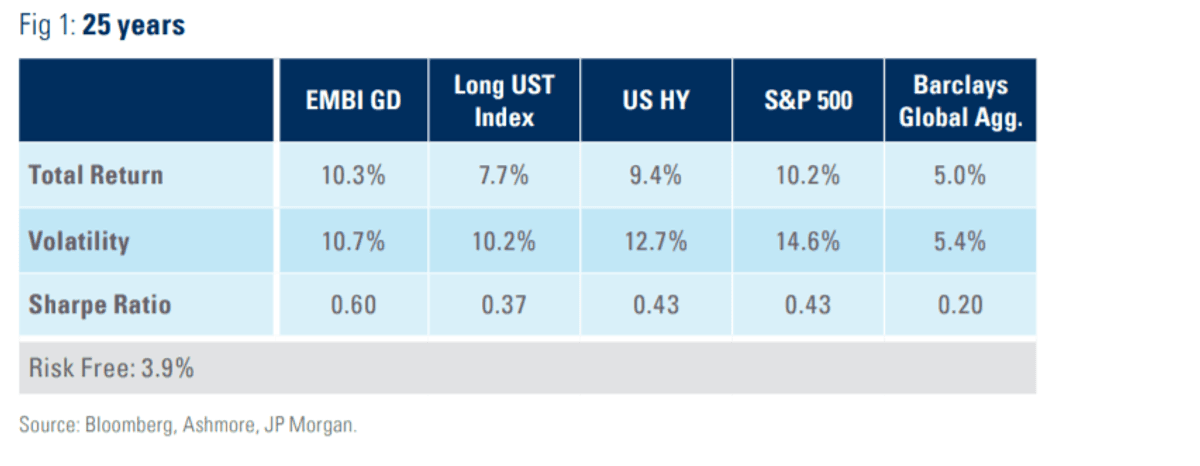

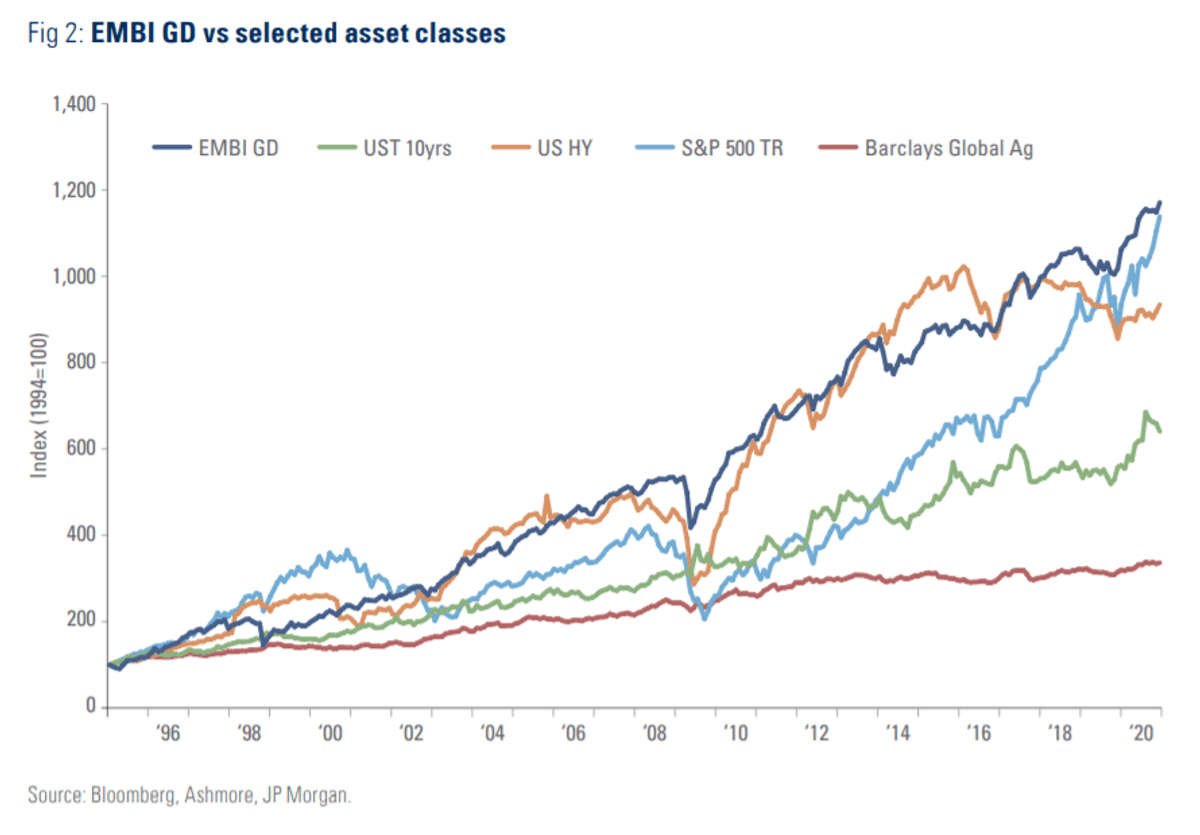

Over the last 25 years, the JP Morgan EMBI Global Diversified, returned 10.3% per year, with a 10.7% volatility, entailing a Sharpe Ratio of 0.60. Both S&P 500 (including dividends reinvestment) and US high yield (HY) bonds delivered similar total returns, but with much higher volatility. Most other equity markets underperformed the EMBI GD.

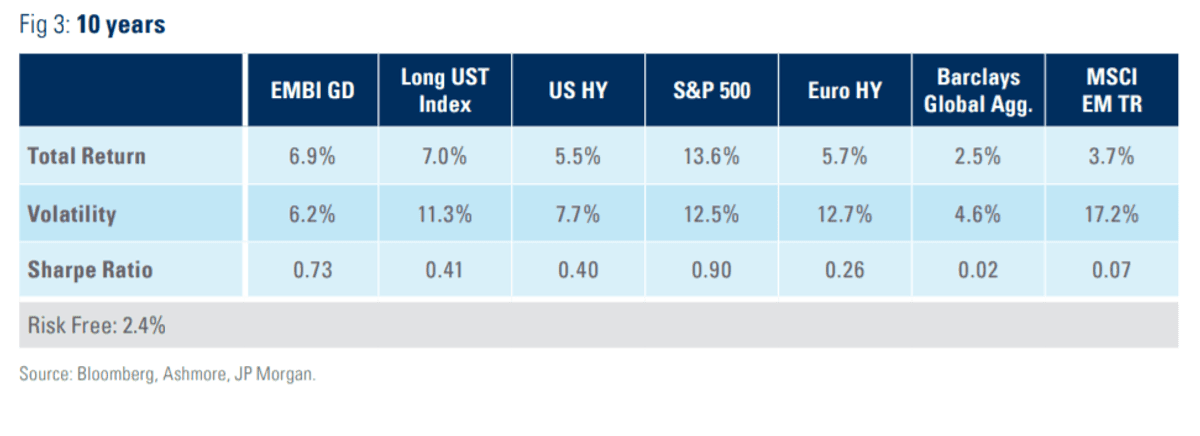

The numbers are a little different over the last ten years as Emerging Markets suffered from a well-documented current account adjustment. A strong US Dollar environment led to outflows in favour of US assets before 2017. However, even in challenging conditions, EM sovereign debt still delivered the best risk-adjusted returns across most asset classes, except for US equities. EM sovereign debt delivered similar results as long-dated US Treasuries, but with almost half the volatility.

Current Valuations

EMBI GD yields have oscillated in a tight 2.60% interval over the past ten years, hitting a low of 4.32% in January 2013 and a high of 7.12% in November 2018. Since this peak in yields, EM sovereign debt saw a healthy 2.35% decline in yield to maturity to 4.78% as of the end of January, only 0.46% above its lowest historical levels. The compensation for credit risk is best assessed in terms of spreads over US Treasury (UST). Similar duration UST were yielding 1.63% as of the end of January, meaning the spread over US on the EMBI GD was 315bp. In simple terms, EM sovereign debt offers almost three times more returns than US Treasuries of the same maturity.

However, last year, a significant amount of bonds from investment-grade countries were included in the index. JP Morgan has changed the inclusion criteria for EM debt indices allowing Saudi Arabia, Bahrain, the United Arab Emirates, Qatar and Kuwait into the EMBI GD from January 2019. Together these countries are now 12.84% of the index. Without them, the spread over US Treasury would be 339bp or 24bp wider than current levels.

Quantifying Long Term Value

The core purpose of this paper is to determine the attractiveness of current valuations in EM sovereign debt. Does the asset class offer a spread over UST that adequately compensates for its credit risk? This question is best answered by examining the odds of default of every single bond in the EMBI GD and multiplying it by the loss given default (haircut in market jargon). Luckily, data is now available for both these metrics.

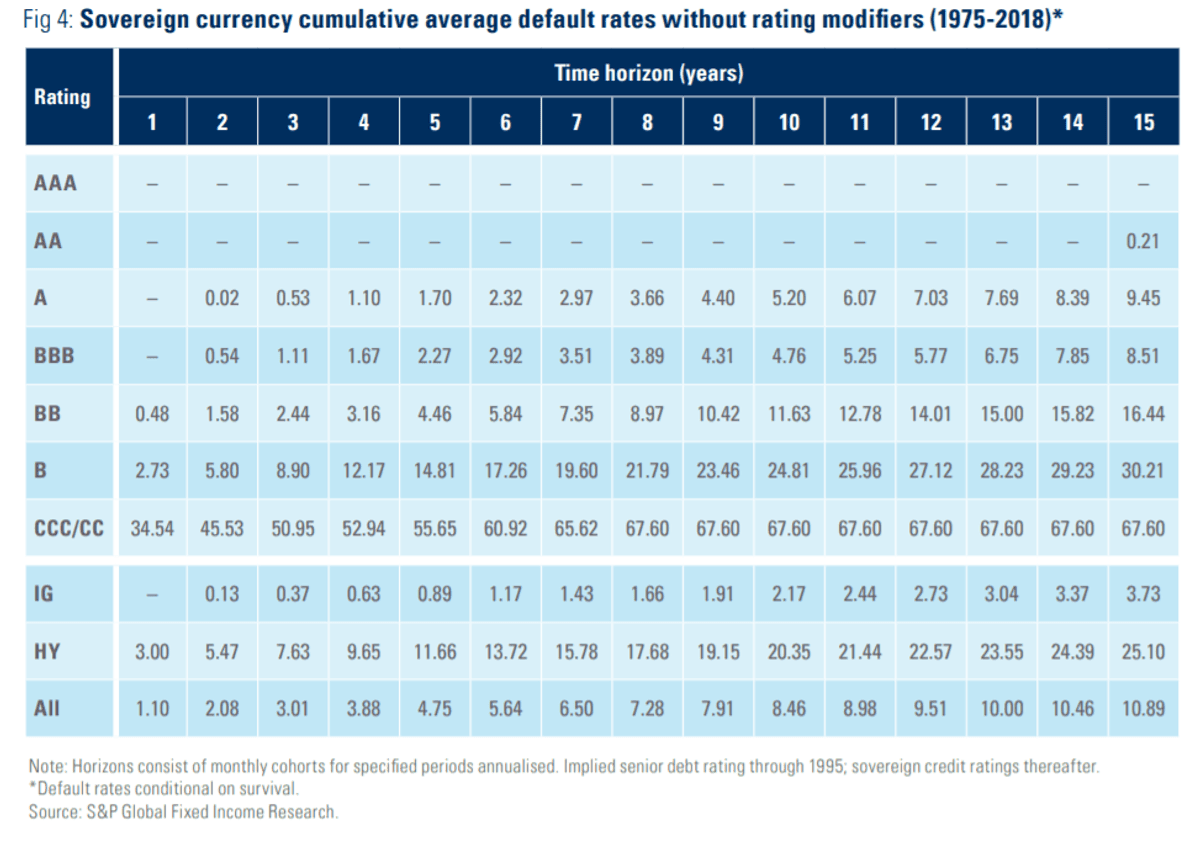

Credit rating agencies reproduce historical default patterns by rating buckets to estimate the likelihood that a country with a specific credit rating will default within a particular time horizon. The table below shows Standard and Poor’s (S&P) future estimate of default probabilities based on 43 years of data. As expected, the lower the credit rating and the longer the maturity of the bond, the higher the likelihood of a credit event:

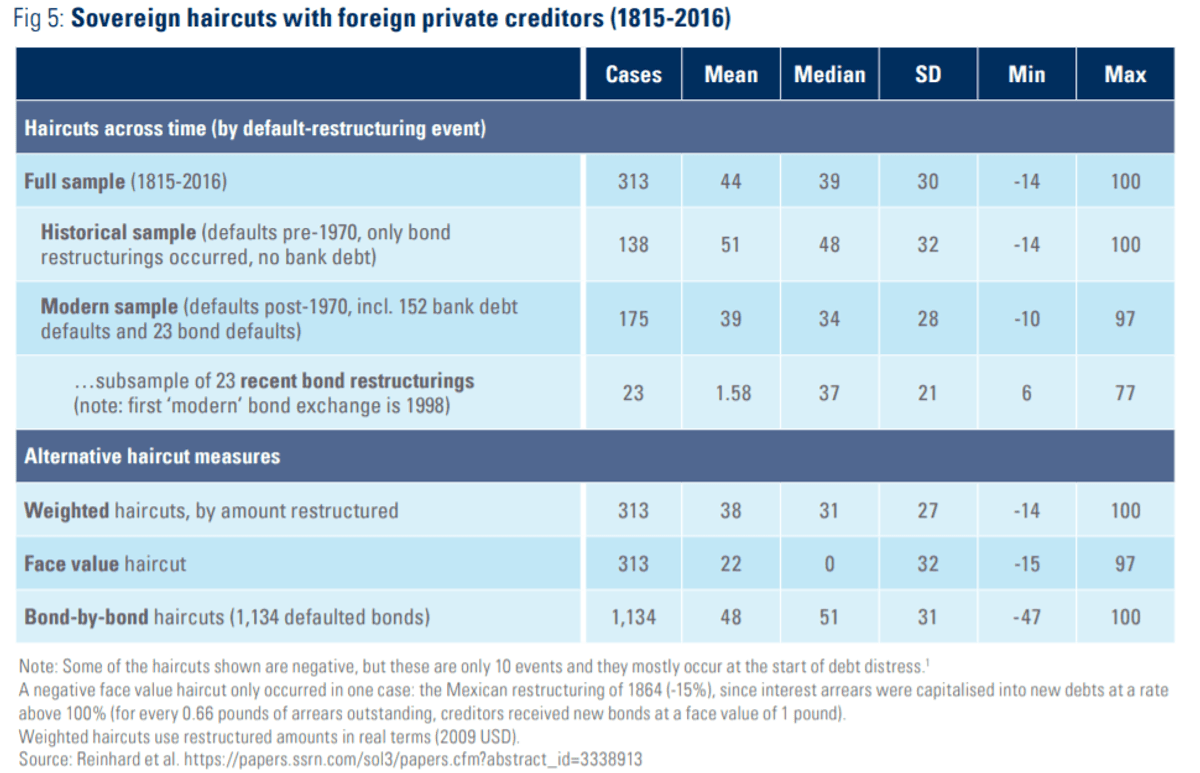

In the past, estimating the true loss associated with sovereign defaults was complicated by poor availability of good quality data for loss given default. However, a recent paper by Carmen Reinhard, Josefin Meyer and Christoph Trebesch shed some light and perspective on the subject. The researchers analysed the recovery value of every single sovereign default since the definitive defeat of Napoleon Bonaparte in the battle of Waterloo in 1815. That was a pivotal moment in history leading to the end of French occupation of Spain and Portugal at a time when the coffers of European powers were depleted by the Napoleonic wars and therefore, had little strength to control their colonies. All Latin American countries, except for Cuba and Puerto Rico, declared independence between 1808 and 1826 enabling them to become (emerging) sovereign issuers in their own right.

Since Waterloo, EM creditors have seen a total of 311 cases of sovereign default, as a few countries defaulted several times. In total, 1,134 bonds have defaulted over this period. The novelty in the Reinhard et al paper is the calculation of the average haircut suffered after defaults. The final investor losses are much more benign than generally assumed. The maximum haircut estimation was 51% when analysing the ‘mean of all defaults pre-1970 without including bank debt’. In a better metric, the ‘median haircut across the full sample’ implies a 39% haircut over the period. However, the economics of the investment universe are best reflected at the ‘median weighted haircut by amount restructured’, in our view. According to this measure, investors in sovereign bonds lost only 31% of the principal amount invested across the last 200 years. This means that sovereign investors recovered, on average, a staggering 69% of their assets after default.

It is, therefore, possible to calculate the expected losses on EM sovereign debt by combining the S&P data on default rate probabilities with the loss given default data from Reinhard et al. For example, a bond with a ‘B’ rating and a maturity of 10 years has a probability of default of 24.8% during its lifespan. When multiplying the odds of default (24.8%) by the loss given default (31%), the expected loss on 10 year ‘B’ bonds is 7.69%. If, for example, 10% of a given portfolio is composed of ‘B’ rated 10-year bonds, then these securities should be expected to generate a 0.77% loss to the portfolio (10% x 7.69%), over 10 years.

Applying this analysis to all the 780 bonds in the EMBI GD, the expected loss for the index varies from 3.6% to 5.9%, depending whether we use the weighted average loss given default of 31% of the highest measure of 51%. Given the average life of the index of 11.4 years, the annual expected loss, in spread terms, is only 31bp to 52bp per year. With spreads on the EMBI GD at 315 bp over UST per year, investors are effectively paid between 6 to 10 times more spread than the expected loss given default for the period. This is obviously far more than required to compensate for liquidity risks or the transaction costs of investing in the asset class.

EM sovereign debt versus US HY: Is it fair to assume they are the same risk premium?

Many investors look at the high correlation between the EMBI GD and US or EU high yield bonds and conclude they already have de facto exposure to EM sovereign debt when buying US or EU HY bonds. Granted, EM sovereign bonds and DM corporate HY bonds tend to respond to the same changes in the macro-environment. They are both inherently connected to the same liquidity cycles that cause boom and bust in credit markets. When liquidity expands, due to significant wealth creation, central bank monetary policy expansions, or indeed both, ‘greedy’ investors will reach for yield across credit markets. On the other hand, when liquidity tightens, ‘fearful’ investors sell assets, leading to increased price volatility.

In spite of these correlations, long term investors should ultimately care about the risk of permanent losses in their portfolio not ephemeral volatility. If one frames risk in terms of the odds of permanent loss given default, rather than volatility it becomes clear that there are fundamental differences between US Corporate HY bonds and EM sovereign bonds. Here are the five major differences:

1) EM sovereign debt offers far greater geographic diversification

Emerging market debt is an asset class that currently comprises more than 70 countries. The EMBI GD alone encompasses 71 countries and 93 quasi-sovereign entities. Only ten years ago, the number of countries in the EMBI GD was 43. The value of this enormous diversification can be harvested by investors as we illustrated in previous papers.

Importantly, every country has unique economic and political structures. Each country goes through its own individual political-institutional reform cycles, which leads to value creation and destruction as well as institutional change. The value of diversification was evident in 2019, when the EMBI GD rose by 15%, in spite of significant mark to market losses in Argentina, Ecuador and Lebanese bonds.

2) Sovereign debt: Obligations assumed by independent states, communities, or political units

Diversification is not the only element distinguishing EM sovereign debt from HY credit markets. An even more important difference is the legal treatment of sovereign debt compared to corporate debt. A corporation is a legal entity generally born to have a limited life span. It will exist while its activities make economic sense. The entire legal framework governing corporates is designed to limit the losses of principal shareholders when companies get into financial trouble. When a company becomes insolvent, governments, employees, creditors and shareholders have recourse to the company’s remaining assets to settle the unpaid liabilities. In respect of unsecured creditors, they generally rank equally with all other unsecured creditors and if there are insufficient assets to share, they may suffer substantial losses.

In contrast a Sovereign is structurally different by virtue of being an independent, political unit. It rarely ceases to exist, unless its entire territory sinks into the ocean or a sudden revolution or war completely changes the political reality of the country. Such risks do exist - for example, creditors to the Romanov dynasty in Russia before the 1917 revolution - but they are exceedingly rare. Sovereign entities generally endure forever, or at least as long as their governments control the territory and hold the authority to tax their population.

The fact that sovereigns exist forever has important implications for bondholders in the eyes of the New York or English Law. When countries default, they usually agree with creditors a framework to restructure their obligations as such countries will want to continue to access the capital markets. If there is no agreement and the state tries to impose a restructure unilaterally, as Argentina did in 2002, bondholders can opt-out (‘hold out’ in the financial jargon) of the exchange offer and sue the country for repayment of the full amount. This legal mechanism explains why the recovery value, after defaults, of sovereign debt is far higher than in corporate debt cases.

3) EM sovereign debt has smaller losses after default than corporate debt

EM sovereign debt offers more than diversification and a better legal structure. The default rates in EM sovereign have been minimal. The default for the EMBI GD has been zero in 13 out of the last 20 years. The worst year since the EMBI GD was created was 2001, when Argentina went under, leading to a default rate of 6.5% of the index. Since then, default rates surpassed 1% only in 2008 (Ecuador), 2014 (Argentina) and 2015 (Ukraine).

By contrast, the weighted average recovery rate for US corporate HY bonds since 1999 has been 36.5%, according to data from Bank of America Merrill Lynch. The average default rate during this period was 7.6%. Default rates peaked at 25.3% in 2002 and 17.8% in 2010 during which years the average recovery value dropped to just 21.7% and 36.6%, respectively.

4) Long term investors have little exposure

Given the extraordinary risk-adjusted return profile, it is our view that EM sovereign debt ought to be a compulsory position for long term investors. Large allocations to EM sovereign should be considered for portfolios with restrictions to equity allocations, such as Central Bank reserve managers, or investors who have to match liabilities, such as insurance companies and pension funds.

Today all anecdotal evidence suggests that these classes of investors have little to no exposure to EM sovereign debt. Central Banks have almost all their reserves in G7 bonds, currently trading in bubbly valuation territory. Some hard data is available for the large US pension plans which publish strategic asset allocation targets and actual positions in annual reports. Their reports suggest the largest pension plans in the country have less than 2% of AUM in EM debt (including sovereign, corporate and local currency bonds), versus a strategic asset allocation of 5-7%. According to efficient frontier studies, even 7% would be too low for this type of investors, in our opinion.

Reining in prejudices and changing allocations takes time. But, as understanding of the significant risk-adjusted returns in EM sovereign debt increases, it is only natural to expect investors gradually to seek larger allocations over the coming years.

5) Limited supply

EM sovereign debt market valuations are likely to be supported by limited supply. After a series of debt crises in the mid and late 1990s, including Mexico in 1995, Asia in 1997, Russia in 1998 and Argentina in 2001, most EM countries have learnt not to borrow too much in US dollars, which, obviously, is a currency they cannot print. Today, around 85% of EM sovereign liabilities are denominated in local currency. Only a few isolated countries like Argentina (and some small frontier countries) still have large amounts of debt denominated in US dollars. As a consequence, they are occasionally reminded of the ‘original sin’ they have committed by not developing local pension systems and yield curves, particularly when political or liquidity crises cause volatility to rise. Going forward, most EM countries will continue to issue mostly in local currency, so the positive technical picture for EM sovereign debt should remain intact.

Summary and Conclusion

EM sovereign debt is the ultimate long-distance runner asset class. It has consistently delivered superior risk-adjusted return owing to excessive credit risk premium priced in the asset class. Defaults are rarer than in US corporate debt and the losses given default are much lower in EM sovereign when compared to US corporate debt.

The asset class has favourable supply-demand technical, offers significant geographic diversification and a better legal framework. Yet, most investors remain structurally underweight in the asset class. We believe they should use any sell-off as an opportunity to go overweight.