Turkey’s local currency markets were widely expected to take a big hit after September’s decision by Moody’s to downgrade the country’s sovereign debt into junk territory.

Shortly after the coup attempt, S&P lowered the country’s credit rating to BB – two notches below investment grade – with a negative outlook. Fitch is the only agency allowing Turkey to cling to an investment grade BBB- rating, but is due to reassess the situation next Spring.

“Three key areas – namely, a sustained slowdown in growth, increasing pressures on external financing and weakening policy predictability - were the focus of the review which had been taking place since 18 July,” noted Muhammet Mercan, senior VP at ING Bank Turkey.

“These were the drivers of the downgrade – the agency cited the increase in the risks related to sizeable external funding requirements and the weakening in previously supportive credit fundamentals, particularly growth and institutional strength, as the main factors behind the decision.”

Mercan added that the rating downgrade will undermine macroeconomic and financial stability, thereby posing major challenges to policymakers given ongoing concerns about the sustainability of strong growth and the current monetary policy position of the CBT.

Normally such political shocks and the ensuing credit downgrades would send local markets into turmoil, but Turkey’s markets showed remarkable resilience. While stocks did fall more than 4% and the yield on the two- year benchmark notes increased to 9% in the aftermath of Moody’s announcement, there was no sign of panic selling or capital flight.

One reason for this is that, with a lot of major infrastructure projects under way, many institutional investors are in Turkey for the long haul, and are unperturbed by short-term instability.

“The country’s demographics, workforce quality and rule of law appear to be stable,” explained Burak Dalgin, managing director at Darby Overseas Investments.

The numbers largely reflect this: while the GDP growth forecast has been revised down from 4.5% to 3.2% for this year, it is still significantly stronger than most similarly sized emerging markets. Two-thirds of it is down to domestic demand, which for many years has been the driving force for the economy. A wide and sophisticated consumer base attracts foreign capital, particularly towards the retail sector.

Another factor, rather paradoxically, is the tactical ‘hot’ money flows from investors that are willing to gamble on high-yield EM bonds as long as there is evidence of stability, even if it turns out to be short-lived.

Some observers expect such capital to be the first to flee. JP Morgan’s data suggests that around US$48bn is held under asset management in Turkish bonds, estimating that as much as US$7bn could leave the markets in forced-selling. So far, though, the Central Bank’s policies have been effective in limiting outflows.

“After the downgrade the CBRT sent a strong signal to investors that it was prepared to compensate any liquidity shortages and meet investors’ needs,” noted Mercan, pointing to the US$3bn decline in the CBRT’s gross reserves.

Following the downgrade in September the banking sector opted to reduce their free holdings at the Central Bank so as to be prepared for any likely liquidity squeeze, generally seen in the quarter-ends.

The lira’s gradual decline, dropping to 3.08 per US dollar from 2.94 on September 22, has caused some concern, but Mercan attributed that to global economic trends, such as the Fed’s potential rate hike and commodity price volatility.

While a weakening lira should improve borrowing costs and boost spending, sub-par currency yield may put off investors.

Finally, consumption – the engine of Turkey’s economy – has slowed recently, increasing by just 5.2% in the second quarter of 2016, far below the 7.2% year- on-year figure originally anticipated.

The government had promised numerous times in the past to reshape the country’s economic model, weaning it off domestic consumption, but, with recent political turmoil still fresh in the minds of policymakers, it is unlikely to continue down such a path. The relative superiority to other EMs, manifested in strong demographics, solid public finances and a debt to GDP ratio at a manageable 26% (substantially lower than most developed economies) allows for some leeway.

“Consumption, though lower, still shows vertical and lateral continuous growth. The recent 30% hike of the minimum wage should encourage it to rise further,” maintained Dalgin.

Furthermore, with food production still lagging behind Europe, farming imports will sustain demand. Finally, public sector credit has risen despite the government pushing up the savings rate, which is another positive sign.

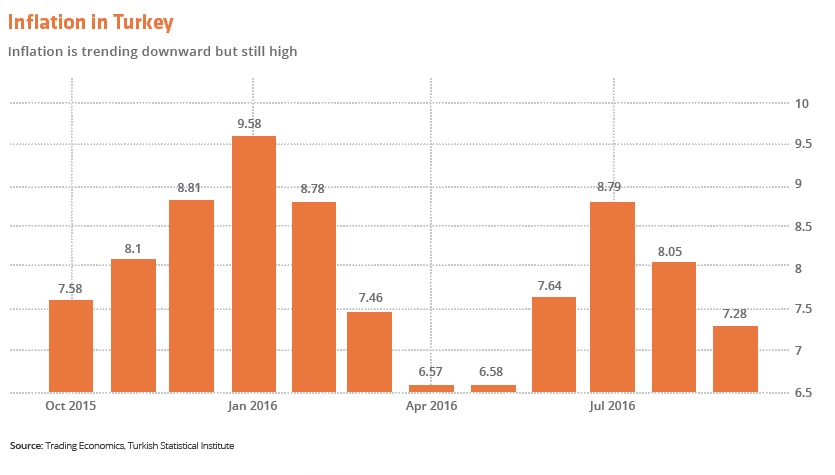

Most observers agree that for now, the MPC’s attention will focus on reviving economic growth, which could result in rising inflation. It currently stands at 8%, although this is slowing.

“So far inflation has not caused too much concern for the Central Bank,” Mercan commented. “Going forward, we don’t expect it to pass into double digits: firstly, as food prices are likely to be supportive and secondly, domestic demand is not strong enough to put pressure on inflation, although we predict that it will remain above the upper band of Central Bank’s target range.”

One danger remains, however. As consumer spending slows, especially in property markets, the banking sector’s over-reliance on deposits could negatively affect liquidity.

With a weak domestic institutional investor base, the burden will fall on foreign capital, which needs to be encouraged through diversification and the development of new funding mechanisms – such as covered bonds and other securities. Whether this will happen remains to be seen.