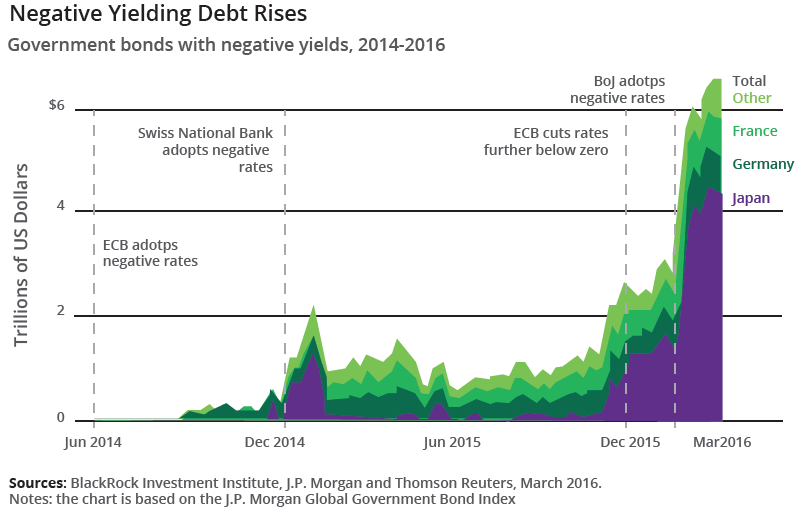

Yields on paper issued by many of the world’s major governments continue to see a flat or negative trend, with few signs of upward pressure easing the minds of global investors. By mid-September, yields on 10-year notes issued by governments of the US, UK, Germany, Switzerland, and Japan stood at 1.729%, 0.908%, 0.073%, -0.380%, and -0.017% respectively.

Many of these countries’ Central Banks have kept rates at astonishing lows. At the time of publishing, the US Fed Funds Rate sat at 0.25-0.5%, the UK’s benchmark interest rate 0.25%, the Eurozone KIR at 0%, Switzerland’s target rate -1.25 - -0.25%, and Japan’s call rate 0-0.10%.

September saw two non-state-backed corporates in Europe issue bonds with a negative yield for the first time: Henkel, a German industrial, commercial and consumer chemical company, issued €500mn in 2-year bonds with a yield of -0.05%, and Sanofi, a French pharmaceuticals manufacturer, issued €1bn in notes maturing in 2020 at the same yield of -0.05%. The notes were rated A2 and A1, respectively.

“The fact that corporate bonds trade with negative yield are prima facie evidence of a bubble in developed market fixed income, in our view. Investors are not paid for credit risk, liquidity risk or duration risk. The universe of negative yielding securities within European investment grade corporates now stands at US$1.2tn. About 55% of the issues with negative yields are in the 1-3-year maturity bucket, while about 25% of the bonds have maturities of 3-5 years,” explains Christian Schniewind, a fixed income portfolio manager at Ashmore, an investment house, in a recent research note.

The “virtuous cycle” in emerging markets, as one fund manager colloquially referred to it, sees lower-for-longer or negative interest rates and easy monetary policy in developed markets send record volumes of inflows into riskier EM assets. In August alone EM credit markets are estimated to have received inflows of US$13.3bn, slightly up from the US$11.2bn of inflows in July and the US$7.4bn in June, according to figures published by the Institute of International Finance (IIF). Investors based in Europe, which has seen among the lowest interest rates globally, accounted for two thirds of all EM fund flows in the three- month run-up to September. Even long-term investors in Japan, traditionally among the most conservative of the bunch, are being swayed to change their tune and target EMs. A source recently tipped that Japan’s Government Pension Investment Fund (GPIF), the world’s largest pension fund, is looking to nearly treble its commitments to emerging markets – partly in a bid to combat mounting losses.

By most accounts, it has been the best year for emerging market credit since 2013, and as the risk-on environment continues to set in, investors are getting more comfortable taking on more risk as price distortions in developed markets continue hitting them where it hurts.

A Virtuous Cycle with Consequences, Good and Bad

Beyond the distortions we have already been seeing in developed market assets – who would have thought investors would have to pay the Swiss government to lend it money? – It could be argued that we are seeing some dislocations in the emerging market world, too.

Of the 66 countries listed in the EMBI diversified index, all except for one have had positive total returns over the year. To some degree, it ignores fundamentals, making relative value a more difficult proposition for portfolio managers, explains Thomas Christiansen, an EM sovereign debt portfolio manager at Nordea Asset Management.

“The first order of price distortions is beginning to hit emerging markets, but it’s largely a factor of what we have seen in developed markets. This is a more extreme distortion of what you are seeing in emerging markets, where you are still seeing positive yields for the most part. One could extrapolate a default probability by taking our yields and maturities and argue that in some places in emerging markets, the default probability is higher than what is actually reflected in the pricing,” Christiansen says.

“On the other hand, you see assets, like bonds issued by Venezuela’s state oil company PDVSA, trade fairly close to their recovery value, particularly on their longer tenors. If you wanted a clear signal of price distortion, you would need to see those bonds trade above recovery value.”

“It ultimately becomes a question of what the market thinks the chances of these countries or companies defaulting on their debt are.”

Some concerns around price distortions hinge on the fact that a great deal of the liquidity being ploughed into emerging market assets is going to ETFs – more than US$38bn since July, to be precise.

These funds tend to be more liquid and easier to trade than actively managed funds or mutual funds. When ETFs are liquidated they are essentially indiscriminate – like a shotgun blast to the market, according to Greg Saichin, CIO Global Emerging Markets Fixed Income at Allianz. Because these portfolios often bid automatically, he believes spreads that are currently tight are likely to become way tighter, and those that are wider, much wider as a result.

Nevertheless, there is a case to be made that easy money has had a positive impact on one of the leading drivers of emerging market performance: commodity prices. Lower interest rates have kept the dollar from appreciating and are fairly supportive for most commodities prices; with the balance between exporters and importers within the EM universe slightly tipped in favour of the former, the result has been a net positive. Despite its ebbs and flows, broad commodity prices – particularly for oil, copper, nickel, and iron ore – are a good deal higher than they were in January despite a blow following the Brexit vote in June.

Sustainability in Question

Is this sustainable, even with a sudden rate hike in the offing? Many would argue flows into emerging markets have been helpful in boosting their fundamentals and growth in real terms. Emerging market growth has slowed on aggregate since 2012, driven in part by a slowdown in China’s economy – which has among other things put a lot of downward pressure on EM equities as a whole. Combined with a steep drop off in the price of commodities since 2014, EM fundamentals have eroded – in some cases more substantially than others.

However, these past few months have seen emerging market growth reach highs not seen for over two years. In October 2014 average real GDP growth across the 30 emerging markets (including China) tracked by the IIF stood at just under 4.6%. By February average growth across these markets was tracking 3%, but by July reached 5.6% before dropping back down to 4.7% in August.

Positive growth dynamics supplemented by improving access to credit is a recipe for more borrowing. With yield hungry investors positioned on the other side of the table. With few signs monetary easing in Europe, the UK or Japan will slow, there seems to be little reason to forecast a strong deviation from the current trend, even with a US rate hike in play, according to Sonja Gibbs, an economist and senior director of the Capital Markets and Emerging Markets Policy Department of the IIF.

The story is similar with EM equities, which have started to track 3-month highs in key emerging markets like Brazil, Peru, and India – though they are looking overvalued by some measures, particularly following the Brexit vote, and are particularly vulnerable to rate hikes.

“If based on valuations to mature markets, both in terms of spreads, prices and earnings, things are looking good. But much of that is predicated on super low rates globally. If you factor any kind of increase in rates, on the other hand, these valuations look stretched – and vulnerable to shocks. The valuation discount is not as striking on the bond side as it is on the equity side,” Gibbs says.

While EM funds have only recently seen larger inflows than DMs as a proportion of assets under management, they still represent a tiny portion of total portfolio allocations – which means beyond periodic upsets and day-to-day shifts in flows, the rally could be here to stay for some time.

“For the most part, people have been relatively under-invested in emerging markets, both on bonds and equities. On the bond front in particular, if you look at the long-term average dating back to 2008, we are still below that in terms of allocation. Equities are way below, if you look at an overall portfolio context,” Gibbs points out. “Given the conditions we are seeing in Europe and Japan, which are looking to continue easing, even a Fed hike is unlikely to deter what could be a fairly prolonged rally.”

“It would really take something like increased political risk, the flaring up of old geopolitical tensions, or a dramatic shift in monetary policy.”

Monetary policy, particularly in Europe and Japan, has been extremely supportive of the EM credit environment so far. Of course, that’s the really the big question here: what happens when the music stops?

“That’s where you get into a discussion about whether helicopter money and coordinated fiscal policy in developed markets keeps it going, or whether this cycle is arrested by the eventual increase in rates or a coordinated divergence from easing. Then the key question really becomes: how efficient has capital allocation become in emerging markets? For the time being, this has been the tide that has lifted all boats, but markets are markets at the end of the day,” Christiansen says.