Background

Background

Since its completion in 2011 Petacalco’s Unit 7, Mexico’s largest power generation complex, has been operating at ~70% of installed capacity due to insufficient coal transport and storage capacity.

To improve the efficiency, CFE, Mexico’s state-owned electric utility, tendered a construction +14-year coal TSA, which was eventually awarded to BlackRock México Infraestructura II.

The LCPL project - based in a region with limited access to natural gas is of great strategic importance to CFE - will enable Petacalco to operate at its full 2,778 MW capacity and provide additional coal storage and transport redundancy.

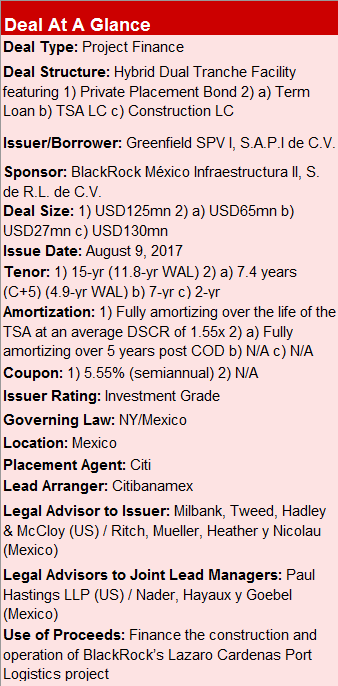

Transaction Breakdown

The construction project consisted of two parallel greenfield and brownfield phases pursuant to lump-sum turn-key EPC contracts with Duro Felguera and Techint, respectively.

To finance these developments, Citi, as the sole Lead Arranger and Placement Agent, provided a fully integrated solution, which involved a hybrid dual-tranche facility featuring a short-term fully amortizing Term Loan, alongside a long-tenor Private Placement.

The innovative structure minimized negative carry, allowing the issuer to monetize the full tenor of the underlying offtaker contract, eliminate refinancing risk, and lock in equity returns from day one. It also incorporated a deal-contingent interest rate swap to hedge LIBOR risk and mitigate breakage costs in the event of an early termination of the TSA.

The Construction LC effectively eliminated construction risk for the note holders, which was a key structural enhancement for the transaction, anticipating investor concerns about the financial stability of local contractors and construction firms, and to achieve investment grade rating despite being a greenfield asset.

Having two very different pools of creditors necessitated structuring and integrating unique documentation requirements to ensure a fully pari passu dual tranche structure. Furthermore, despite concerns about institutional investors’ growing reluctance to participate in coal-related transactions, targeted distribution allowed to reach the likely purchasers (many of whom made their first foray into Mexico) and achieve an oversubscription rate of 1.5x.

The deal was a first ever placement of a 4(a)(2) project bond in Latin America, incorporating a long (11-month) delayed-draw feature - very rare outside the US - for a fully contracted asset under construction. The deal achieved tightest spread for a CFE-related project bond financing.

As the first truly non-recourse private placement for a greenfield asset in Latin America, the issuance will open a new market for future Latin American greenfield issuers.